Effective saving strategies are the cornerstone of financial security, empowering individuals to build a brighter future. This comprehensive guide explores a range of proven methods to help you navigate the world of saving, investing, and financial planning. From understanding your current financial situation to setting realistic goals and automating savings, we’ll delve into practical strategies that can transform your relationship with money.

By embracing these principles, you’ll gain valuable insights into managing your finances effectively, achieving your financial aspirations, and building a strong foundation for long-term financial well-being.

Understanding Your Financial Situation: Effective Saving Strategies

Before embarking on any saving strategy, it’s crucial to gain a comprehensive understanding of your current financial standing. This involves analyzing your income, expenses, and debt obligations. A clear picture of your financial situation serves as the foundation for setting realistic saving goals and developing effective strategies to achieve them.

Creating a Detailed Personal Budget

A personal budget acts as a roadmap for your finances, outlining your income and expenses. It helps you identify areas where you can cut back and allocate funds towards savings.To create a comprehensive budget, follow these steps:

- Track your income:Record all sources of income, including salary, investments, and any other regular payments you receive. This will provide a clear picture of your total income.

- Track your expenses:Keep a detailed record of all your expenses, categorizing them into essential needs, discretionary spending, and debt payments. This involves tracking both fixed expenses like rent and utilities, and variable expenses like groceries and entertainment.

- Analyze your spending habits:Once you have a comprehensive record of your income and expenses, analyze your spending patterns. Identify areas where you can potentially cut back or adjust your spending habits. For instance, consider reducing your eating out expenses, negotiating lower bills, or finding alternative entertainment options.

- Create a budget plan:Based on your income and expense analysis, create a budget plan that allocates your income towards essential expenses, savings, and debt payments. This plan should be realistic and achievable, taking into account your financial goals and priorities.

Tracking Income and Expenses

Accurate tracking of income and expenses is essential for creating an effective budget. This can be achieved through various methods:

- Spreadsheet:Utilize a spreadsheet program like Microsoft Excel or Google Sheets to manually track your income and expenses. This allows for detailed categorization and analysis of your spending patterns.

- Budgeting apps:Numerous budgeting apps are available for smartphones and computers. These apps automate the process of tracking your income and expenses, providing insights into your spending habits and offering personalized recommendations.

- Financial management software:More comprehensive financial management software can track your income, expenses, and investments, offering a holistic view of your financial situation. These programs typically integrate with your bank accounts and credit cards for automated data entry.

Identifying and Analyzing Spending Habits

Understanding your spending habits is crucial for identifying areas where you can save money. Analyze your expense categories to determine which areas consume the most of your budget.

“The key to successful saving is to understand where your money goes and identify areas where you can cut back or adjust your spending habits.”

Managing Debt Effectively

Debt can significantly impact your ability to save. Effective debt management is essential for freeing up funds for savings and improving your overall financial health.

- Create a debt repayment plan:Prioritize your debts based on interest rates and repayment terms. Focus on paying down high-interest debts first, as these can accrue significant interest charges over time.

- Negotiate lower interest rates:Contact your creditors to explore options for lowering interest rates on your loans. This can significantly reduce the overall cost of your debt and free up more funds for savings.

- Consider debt consolidation:If you have multiple high-interest debts, consider consolidating them into a single loan with a lower interest rate. This can simplify your repayment process and potentially reduce your monthly payments.

- Avoid accumulating new debt:Once you have started managing your debt effectively, avoid accumulating new debt. This will allow you to focus on paying down existing debt and building your savings.

Setting Realistic Financial Goals

Having a clear understanding of your current financial situation is the first step towards effective saving. The next step is to set realistic financial goals. These goals will serve as a roadmap, guiding your saving efforts and motivating you to stay on track.

Defining Financial Goals

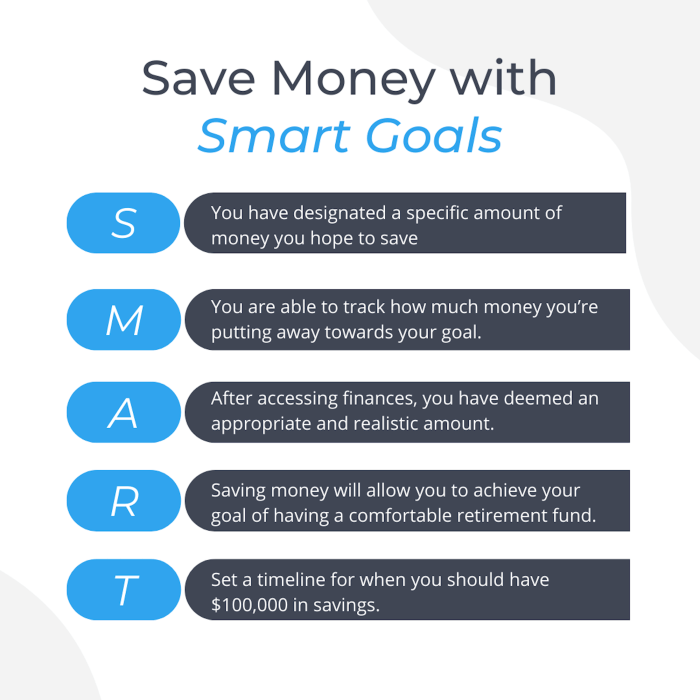

Financial goals are specific, measurable, achievable, relevant, and time-bound (SMART) objectives that you aim to achieve with your savings. They provide direction and purpose to your saving journey, helping you stay focused and motivated.

Types of Financial Goals

Financial goals can be categorized into short-term, mid-term, and long-term goals, based on their time horizon.

- Short-term goals:These are goals that you aim to achieve within a year or less. Examples include saving for a vacation, a down payment on a new car, or a new laptop.

- Mid-term goals:These goals typically have a time horizon of one to five years. Examples include saving for a home renovation, a wedding, or a child’s education.

- Long-term goals:These are goals that you aim to achieve over five years or more. Examples include saving for retirement, a down payment on a house, or a significant investment.

The Importance of Goal Setting

Setting financial goals is crucial for effective saving.

- Motivation:Having specific goals gives you a clear reason to save and motivates you to stick to your saving plan.

- Focus:Goals help you prioritize your spending and allocate your savings effectively.

- Discipline:Knowing what you are saving for can help you stay disciplined and avoid unnecessary spending.

- Tracking Progress:Goals provide a framework for tracking your progress and celebrating your achievements along the way.

Automating Savings

Automating your savings is a powerful strategy that can help you consistently save money without having to think about it. By setting up automatic transfers from your checking account to your savings account, you can take the guesswork out of saving and ensure that you’re making progress towards your financial goals.

Setting Up Automatic Savings Transfers

Setting up automatic savings transfers is simple and can be done through your online banking platform. Here’s how:

- Log in to your online banking account.

- Navigate to the “Transfers” or “Bill Pay” section.

- Select “Create a New Transfer” or “Add a Bill Payer.”

- Choose your checking account as the source account and your savings account as the destination account.

- Specify the amount you want to transfer and the frequency (e.g., weekly, bi-weekly, monthly).

- Confirm the transfer details and set a start date.

Advantages of Automating Savings

Automating savings offers numerous benefits:

- Consistency:Automatic transfers ensure that you save regularly, regardless of your busy schedule or forgetfulness.

- Discipline:By automating savings, you’re less likely to spend money that you’ve already earmarked for your savings goals.

- Time-Saving:You don’t have to manually transfer money, freeing up your time for other tasks.

- Compounding Growth:The earlier you start saving, the more time your money has to grow through compounding interest.

- Goal-Oriented:Automating savings can help you stay focused on your financial goals and track your progress.

“Automating your savings is like setting up a recurring payment for your future self.”

Exploring Savings Options

Once you understand your financial situation and have set realistic financial goals, you need to explore the various savings options available to you. Choosing the right savings account can significantly impact your financial progress.

Types of Savings Accounts

Different types of savings accounts offer varying features and benefits. Understanding these differences can help you choose the option that best suits your needs.

- High-Yield Savings Accounts (HYSA): These accounts offer higher interest rates than traditional savings accounts. They are a good option for those looking to maximize their returns while maintaining easy access to their funds. However, they may have higher minimum balance requirements.

- Money Market Accounts (MMAs): These accounts offer a higher interest rate than traditional savings accounts and may provide limited check-writing privileges. They typically require a higher minimum balance than HYSAs.

- Certificates of Deposit (CDs): CDs offer a fixed interest rate for a specific term. The interest rate is typically higher than HYSAs and MMAs, but you cannot access your funds until the term ends. This makes them suitable for long-term savings goals.

Comparison of Savings Options

The table below provides a comparison of the key features, benefits, and drawbacks of each savings option:

| Account Type | Interest Rate | Minimum Balance | Withdrawal Restrictions |

|---|---|---|---|

| High-Yield Savings | Typically higher than traditional savings accounts | May vary, but generally lower than MMAs | Limited withdrawals, usually a few per month |

| Money Market Account | Higher than traditional savings accounts, but may fluctuate | Higher than HYSAs | May allow limited check-writing privileges |

| Certificate of Deposit (CD) | Highest among savings options, but fixed for the term | May vary, but generally higher than HYSAs and MMAs | Funds are locked in for the term, early withdrawal penalties apply |

Emergency Funds

An emergency fund is a crucial component of financial security. It acts as a safety net to cover unexpected expenses such as medical bills, job loss, or car repairs.

An emergency fund should ideally cover 3-6 months of essential living expenses.

Having an emergency fund can prevent you from going into debt or depleting your savings during unexpected events.

Investing for Growth

Investing is the process of allocating money to assets with the expectation of generating a positive return. This return can come in the form of interest, dividends, or capital appreciation. Investing is crucial for long-term wealth accumulation as it allows your money to grow over time, potentially outpacing inflation and helping you reach your financial goals.

Understanding Different Investment Options

Investing involves allocating your money to different assets with the potential to generate returns. The most common investment options include:

- Stocks: Represent ownership in a company. When you buy a stock, you become a shareholder in the company, and you are entitled to a share of its profits. Stocks are considered a higher-risk investment, but they also have the potential for higher returns.

Stock prices fluctuate based on factors such as company performance, industry trends, and overall market sentiment.

- Bonds: Represent loans made to a company or government. When you buy a bond, you are lending money to the issuer, and they promise to pay you back with interest. Bonds are generally considered a lower-risk investment than stocks, but they also have lower potential returns.

Bond prices are influenced by interest rates, inflation, and the creditworthiness of the issuer.

- Mutual Funds: Pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They are managed by professional fund managers who aim to achieve specific investment objectives. Mutual funds provide diversification and professional management, making them a suitable option for investors with limited time or expertise.

- Exchange-Traded Funds (ETFs): Similar to mutual funds, but they trade on stock exchanges like individual stocks. ETFs offer diversification and lower expense ratios compared to traditional mutual funds. They are often used to track specific market indexes, sectors, or commodities.

Risk and Return Considerations

Every investment carries a certain level of risk, and the potential return is directly related to the risk level. Higher-risk investments, such as stocks, have the potential for higher returns but also carry a greater chance of losing money. Lower-risk investments, such as bonds, generally offer lower returns but are less likely to lose value.

Risk and return are inherently linked.Higher potential returns usually come with higher risk, and vice versa.

The Importance of Diversification

Diversification is a crucial investment strategy that involves spreading your money across different asset classes, sectors, and geographies. This reduces the overall risk of your portfolio by mitigating the impact of any single investment performing poorly.

- Asset Allocation: Involves dividing your portfolio among different asset classes, such as stocks, bonds, real estate, and commodities. This helps to balance risk and return based on your investment goals and risk tolerance.

- Sector Diversification: Involves investing in companies from different industries, such as technology, healthcare, or energy. This reduces the risk of your portfolio being heavily impacted by a downturn in a specific industry.

- Geographic Diversification: Involves investing in companies from different countries. This helps to reduce the impact of economic or political instability in a particular region.

Retirement Planning

Retirement planning is an essential aspect of financial well-being, and starting early is crucial to securing a comfortable future. A well-defined retirement plan allows you to accumulate wealth over time, ensuring financial independence and security during your golden years.

Retirement Savings Options

There are several retirement savings options available, each with its own set of features, tax benefits, and contribution limits. Understanding these options is vital to making informed decisions about your retirement savings strategy.

- 401(k): Offered by employers, a 401(k) is a defined-contribution retirement plan that allows pre-tax contributions to be deducted from your paycheck and invested in a variety of assets, such as stocks, bonds, and mutual funds. These contributions grow tax-deferred, meaning you won’t pay taxes until you withdraw the funds in retirement.

The maximum contribution limit for 2023 is $22,500 for individuals under age 50 and $30,000 for those 50 and over.

- Traditional IRA: A traditional IRA is a retirement savings plan that allows individuals to contribute pre-tax dollars, which grow tax-deferred. You can deduct contributions from your taxable income, reducing your current tax liability. However, withdrawals in retirement are taxed as ordinary income.

The maximum contribution limit for 2023 is $6,500 for individuals under age 50 and $7,500 for those 50 and over.

- Roth IRA: A Roth IRA is a retirement savings plan that allows individuals to contribute after-tax dollars, which grow tax-free. This means you will not pay taxes on withdrawals in retirement. While contributions are not tax-deductible, withdrawals in retirement are tax-free, making it an attractive option for individuals who expect to be in a higher tax bracket in retirement.

The maximum contribution limit for 2023 is $6,500 for individuals under age 50 and $7,500 for those 50 and over.

Tax Implications and Benefits

The tax implications and benefits of each retirement savings plan vary significantly, making it crucial to understand these differences when choosing the best option for your individual needs.

- 401(k): Contributions are pre-tax, reducing your taxable income and current tax liability. However, withdrawals in retirement are taxed as ordinary income. Some employers may offer matching contributions, which can significantly boost your retirement savings.

- Traditional IRA: Contributions are pre-tax, reducing your taxable income and current tax liability. However, withdrawals in retirement are taxed as ordinary income. Individuals with lower current incomes may benefit from the tax deduction in the present, while those expecting higher incomes in retirement might prefer a Roth IRA.

- Roth IRA: Contributions are after-tax, meaning you won’t receive a tax deduction in the present. However, withdrawals in retirement are tax-free, making it an attractive option for individuals who expect to be in a higher tax bracket in retirement.

Compound Interest and Retirement Savings

Compound interest is a powerful tool for retirement savings. It allows your money to grow exponentially over time by earning interest on both the principal amount and accumulated interest.

Compound Interest Formula:A = P(1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

For example, if you invest $10,000 at an annual interest rate of 7% compounded annually for 30 years, your investment will grow to approximately $76,122.55. This demonstrates the power of compound interest, allowing your savings to grow significantly over time.

Smart Spending Habits

While saving is crucial for achieving financial goals, smart spending habits play an equally important role. By making conscious choices about how you spend your money, you can significantly reduce unnecessary expenses and free up more funds for saving and investing.

This section will explore practical tips for reducing overspending and maximizing your savings.

Identifying Common Areas of Overspending

Overspending can occur in various areas of life. Understanding where your money is going is the first step toward controlling your spending. Here are some common areas where people tend to overspend:

- Dining Out:Frequent restaurant visits can quickly drain your budget. Consider cooking more meals at home and limiting dining out to special occasions.

- Impulse Purchases:Unplanned purchases, often triggered by emotions or advertising, can lead to significant overspending. Take time to reflect before making a purchase, especially for non-essential items.

- Subscription Services:Streaming services, gym memberships, and other subscriptions can add up quickly. Regularly review your subscriptions and cancel those you no longer use or find less valuable.

- Entertainment:Movies, concerts, and other entertainment activities can be expensive. Look for free or affordable alternatives, such as local events, parks, and libraries.

- Shopping Habits:Frequent shopping trips, especially for non-essentials, can lead to overspending. Consider setting a budget for shopping and sticking to it.

Strategies for Curbing Overspending, Effective saving strategies

Once you’ve identified your areas of overspending, you can implement strategies to curb these habits. Here are some effective approaches:

- Create a Budget:A budget helps you track your income and expenses, allowing you to identify areas where you can cut back. Use budgeting apps or spreadsheets to track your spending and make adjustments as needed.

- Use the 30-Day Rule:Before making a non-essential purchase, wait 30 days. If you still want the item after that period, you’re more likely to make an informed decision.

- Negotiate Prices:Don’t be afraid to negotiate prices, especially for larger purchases like cars or appliances. Research average prices and be prepared to walk away if you don’t get a fair deal.

- Shop Around for Deals:Compare prices from different retailers and look for discounts, coupons, and cashback offers. Consider buying used items or refurbished products to save money.

- Cook at Home More Often:Eating out can be expensive. Prepare meals at home to save money and control the ingredients and portions.

- Limit Spending on Entertainment:Explore free or affordable entertainment options, such as visiting museums on free days, attending local events, or enjoying outdoor activities.

Prioritizing Needs Over Wants

A fundamental principle of smart spending is prioritizing needs over wants. Needs are essential items that you require for survival or basic functioning, such as food, shelter, healthcare, and transportation. Wants, on the other hand, are items that are desirable but not essential.

By focusing on your needs and limiting spending on wants, you can free up more resources for saving and investing. This approach requires discipline and a willingness to delay gratification, but it can have a significant impact on your financial well-being.

Mindful Spending

Mindful spending involves making conscious and deliberate choices about how you spend your money. It goes beyond simply tracking your expenses; it’s about understanding your spending patterns, identifying your values, and aligning your spending with your financial goals.

By practicing mindful spending, you can make more informed purchasing decisions and avoid impulse buys. This approach can help you reduce unnecessary expenses and achieve your financial objectives more effectively.

Seeking Professional Advice

Navigating the complex world of personal finance can be overwhelming, especially when it comes to crafting an effective savings strategy. Seeking professional advice from a qualified financial advisor can provide invaluable guidance and support, empowering you to make informed decisions and achieve your financial goals.

A financial advisor acts as your trusted guide, providing personalized financial advice tailored to your unique circumstances and aspirations. They can help you develop a comprehensive savings plan, navigate investment options, and make strategic decisions to secure your financial future.

Benefits of Consulting a Financial Advisor

Consulting a financial advisor offers a multitude of benefits that can significantly enhance your savings journey. Here are some key advantages:

- Personalized Financial Guidance:A financial advisor takes the time to understand your financial situation, goals, risk tolerance, and time horizon. They use this information to create a customized plan that aligns with your specific needs and aspirations.

- Comprehensive Savings Plan Development:Financial advisors possess the expertise to develop a comprehensive savings plan that encompasses various aspects of your financial life, including budgeting, debt management, investment strategies, and retirement planning.

- Objective Perspective:It’s easy to get caught up in emotions when making financial decisions. A financial advisor provides an objective perspective, helping you avoid impulsive choices and make rational decisions based on sound financial principles.

- Access to Expertise:Financial advisors have extensive knowledge and experience in financial markets, investment strategies, and tax laws. They can provide valuable insights and guidance on complex financial matters.

- Accountability and Support:Having a financial advisor can provide accountability and support throughout your savings journey. They can help you stay on track with your goals, address any challenges that arise, and provide ongoing guidance and encouragement.

How a Financial Advisor Can Assist

Financial advisors can play a crucial role in helping you develop a comprehensive savings plan that aligns with your goals and aspirations. Here are some key ways they can assist:

- Financial Planning and Budgeting:Financial advisors can help you create a realistic budget that reflects your income, expenses, and savings goals. They can also provide guidance on managing debt and optimizing your cash flow.

- Investment Strategy Development:Financial advisors can help you develop an investment strategy that aligns with your risk tolerance, time horizon, and financial goals. They can guide you on choosing appropriate investments, diversifying your portfolio, and managing risk.

- Retirement Planning:Retirement planning is a crucial aspect of long-term financial security. Financial advisors can help you estimate your retirement needs, choose suitable retirement savings vehicles, and develop a plan to ensure a comfortable retirement.

- Tax Planning:Financial advisors can help you optimize your tax situation by leveraging tax-advantaged savings accounts, taking advantage of deductions and credits, and minimizing your tax liability.

- Estate Planning:Financial advisors can assist you with estate planning, including creating a will, setting up trusts, and ensuring your assets are distributed according to your wishes.

Choosing a Financial Advisor

Selecting the right financial advisor is crucial to ensure you receive the best possible guidance and support. Here are some factors to consider when choosing a financial advisor:

- Credentials and Experience:Look for financial advisors who hold relevant professional certifications, such as Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), or Certified Public Accountant (CPA). Consider their experience in working with clients similar to you.

- Fees and Services:Understand the advisor’s fee structure, which can vary based on their services and the amount of assets they manage. Discuss their fees upfront and ensure they align with your budget.

- Communication Style and Compatibility:It’s important to feel comfortable and confident communicating with your financial advisor. Choose someone who listens attentively, explains concepts clearly, and is responsive to your questions and concerns.

- References and Reviews:Ask for references from previous clients and check online reviews to get insights into the advisor’s reputation and client satisfaction.

- Fiduciary Duty:Ensure the financial advisor acts as a fiduciary, meaning they are legally obligated to put your interests first. This ensures they provide unbiased advice and act in your best financial interests.

Last Point

Embarking on the journey of effective saving strategies is a powerful step toward financial freedom and peace of mind. By taking control of your finances, setting realistic goals, and implementing the strategies Artikeld in this guide, you’ll be well-equipped to secure your future and unlock the potential for a more prosperous life.

Detailed FAQs

What are some common mistakes people make when saving?

Common saving mistakes include not having a budget, not saving consistently, spending impulsively, and not seeking professional advice.

How much should I save each month?

The ideal savings rate varies depending on individual circumstances, financial goals, and risk tolerance. A general rule of thumb is to aim for 15-20% of your income.

Is it better to save or invest?

Both saving and investing are crucial for financial security. Saving provides a safe haven for emergency funds and short-term goals, while investing offers the potential for long-term growth.