How to manage debt is a crucial skill for financial well-being. Debt can be a powerful tool, but if left unchecked, it can quickly spiral out of control, leading to stress, financial instability, and even legal issues. This guide provides a comprehensive approach to understanding your debt, creating a manageable plan, and building healthy financial habits.

From the basics of identifying different debt types and their consequences to navigating the complexities of negotiation and seeking professional help, we will explore practical strategies for taking control of your finances and achieving financial freedom.

Understanding Your Debt

Taking control of your debt starts with understanding it. Knowing the different types of debt, the potential consequences of not managing it, and how to track it effectively is crucial to developing a successful debt management strategy.

Types of Debt

Different types of debt come with different terms and conditions, affecting how they impact your financial situation.

- Credit Card Debt:This is a revolving debt, meaning you can borrow money repeatedly up to a certain limit. It often has high interest rates, making it one of the most expensive forms of debt.

- Student Loans:These loans are specifically for financing education. They usually have lower interest rates than credit cards but can accumulate over time, depending on the repayment plan chosen.

- Mortgages:A mortgage is a loan used to purchase a home. It’s typically a long-term loan with a fixed or adjustable interest rate.

- Personal Loans:These are unsecured loans used for various purposes, such as home improvements or medical expenses. They generally have higher interest rates than secured loans like mortgages.

- Payday Loans:These are short-term, high-interest loans designed to bridge a gap until your next paycheck. They can quickly become a debt trap due to their high interest rates and fees.

Consequences of Unmanaged Debt, How to manage debt

Failing to manage debt can have serious financial consequences.

- Late Payments:Missing payments can result in late fees, damage your credit score, and potentially lead to account closure.

- Collection Agencies:If you default on your debt, it may be sold to a collection agency, which can aggressively pursue repayment and potentially damage your credit score.

- Legal Action:In some cases, creditors can take legal action to recover unpaid debts, including wage garnishment or property seizure.

- Stress and Anxiety:The weight of unmanaged debt can cause significant stress and anxiety, impacting your mental and emotional well-being.

Tracking Your Debt

Keeping track of your debt is crucial for effective management.

- List All Debts:Make a comprehensive list of all your debts, including the amount owed, interest rate, minimum payment, and due date.

- Use a Debt Tracker:Utilize a spreadsheet, budgeting app, or debt tracking website to monitor your debts and progress.

- Review Regularly:Review your debt tracker periodically to ensure accuracy and identify any potential issues.

“Understanding your debt is the first step towards taking control of your finances.”

Creating a Debt Management Plan

A debt management plan is a roadmap for tackling your debt effectively. It Artikels how you will prioritize, allocate funds, and ultimately eliminate your debt. This plan requires a deep understanding of your financial situation, and a willingness to make necessary changes to your spending habits.

Creating a Budget

A budget is the foundation of any successful debt management plan. It provides a clear picture of your income and expenses, allowing you to identify areas where you can cut back and free up funds for debt repayment.

- Track your income and expenses.Record every dollar you earn and spend for a month to gain an accurate understanding of your financial picture. You can use a spreadsheet, budgeting app, or even a simple notebook.

- Categorize your expenses.Organize your expenses into categories like housing, food, transportation, entertainment, and debt payments. This helps you identify areas where you can reduce spending.

- Identify areas for savings.Look for opportunities to reduce unnecessary expenses. For example, can you cook more meals at home instead of eating out? Can you find a cheaper gym membership? Can you cut down on subscriptions you don’t use?

- Allocate funds for debt repayment.Once you’ve identified areas for savings, allocate a specific amount of money each month to your debt repayment.

Prioritizing Debt Repayment

Once you have a budget in place, you need to prioritize which debts to tackle first. Two popular methods are the debt snowball and debt avalanche methods.

Debt Snowball Method

The debt snowball method focuses on paying off the smallest debt first, regardless of interest rate. The idea is to gain momentum and motivation by quickly eliminating debts.

- List your debts from smallest to largest balance.

- Make minimum payments on all debts except the smallest one.

- Put all extra money towards the smallest debt.

- Once the smallest debt is paid off, roll that payment amount into the next smallest debt.

- Continue this process until all debts are paid off.

Debt Avalanche Method

The debt avalanche method prioritizes paying off debts with the highest interest rates first. This method saves you the most money in the long run by minimizing the amount of interest you pay.

- List your debts from highest interest rate to lowest.

- Make minimum payments on all debts except the one with the highest interest rate.

- Put all extra money towards the debt with the highest interest rate.

- Once that debt is paid off, roll that payment amount into the next highest interest rate debt.

- Continue this process until all debts are paid off.

Consolidating or Refinancing Debt

Consolidating or refinancing debt can be a useful strategy for managing debt, but it’s important to understand the potential benefits and drawbacks.

Debt Consolidation

Debt consolidation involves combining multiple debts into a single loan with a new interest rate and repayment term.

- Benefits:Simplifying your payments, potentially lowering your monthly payments, and potentially getting a lower interest rate.

- Drawbacks:May extend the repayment term, leading to paying more interest over time. May not be suitable for everyone, especially those with poor credit scores.

Debt Refinancing

Debt refinancing involves replacing an existing loan with a new one with different terms, such as a lower interest rate or a longer repayment term.

- Benefits:Potentially lowering your monthly payments, potentially getting a lower interest rate.

- Drawbacks:May extend the repayment term, leading to paying more interest over time. May not be suitable for everyone, especially those with poor credit scores.

Important Note:Before consolidating or refinancing debt, carefully consider the terms of the new loan, including the interest rate, repayment term, and any associated fees. It’s also essential to ensure that you can afford the new monthly payments.

Negotiating with Creditors: How To Manage Debt

Negotiating with creditors can be a crucial step in managing your debt effectively. By proactively engaging with your creditors, you can potentially reduce your overall debt burden and make your repayment journey more manageable. This section will delve into strategies for negotiating with creditors and explore options such as debt settlement and debt relief programs.

Negotiating Lower Interest Rates or Payment Plans

Negotiating with creditors can help you secure more favorable terms, potentially reducing your overall interest payments and making your debt more manageable. Here are some tips for negotiating with creditors:

- Be polite and respectful: When communicating with creditors, maintain a professional and courteous tone. This approach can foster a more positive and productive dialogue.

- Document your financial situation: Gather documentation that illustrates your current financial circumstances, such as your income, expenses, and any recent changes that might have impacted your ability to make payments.

- Be prepared to make a proposal: Before initiating a negotiation, have a clear idea of what you are seeking. For example, you might propose a lower interest rate, a temporary reduction in monthly payments, or a combination of both.

- Be willing to compromise: While it’s important to advocate for your needs, be open to compromise. Creditors are more likely to negotiate if they see you are willing to work towards a mutually agreeable solution.

- Consider a debt consolidation loan: A debt consolidation loan can help you simplify your debt management by combining multiple debts into a single loan with a potentially lower interest rate.

Debt Settlement or Debt Relief Programs

Debt settlement and debt relief programs offer alternative approaches to managing overwhelming debt. These programs typically involve negotiating with creditors to reduce the amount of debt you owe.

- Debt Settlement: Debt settlement programs involve working with a third-party company that negotiates with your creditors on your behalf. These companies typically collect a fee for their services.

- Debt Relief Programs: Debt relief programs often involve a combination of strategies, such as debt consolidation, debt settlement, and credit counseling. These programs can provide guidance and support as you work towards managing your debt.

Maintaining Open Communication with Creditors

Maintaining open and honest communication with your creditors is essential for managing your debt effectively. Here are some key points to consider:

- Be proactive: Don’t wait until you’re behind on payments to contact your creditors. If you anticipate a potential challenge in making payments, reach out to them early to discuss options.

- Keep detailed records: Maintain a record of all your communications with creditors, including dates, times, and the content of your conversations. This documentation can be helpful if any disputes arise.

- Be truthful and transparent: Be honest with your creditors about your financial situation. They are more likely to work with you if they understand your circumstances.

Building Good Financial Habits

Once you have a solid debt management plan in place, it’s crucial to build good financial habits that will help you avoid accumulating debt in the future. This involves understanding your spending patterns, setting realistic budgets, and prioritizing saving.

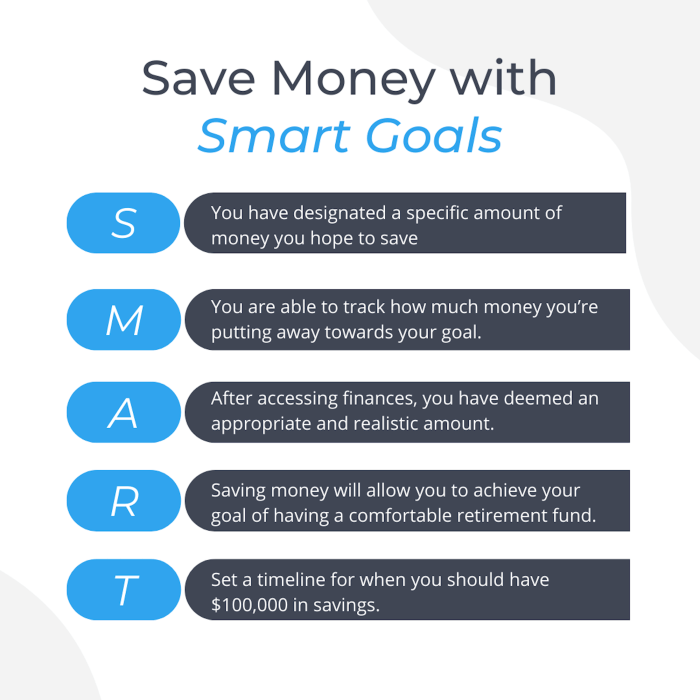

Saving Money and Building an Emergency Fund

Saving money is essential for financial stability and can help you avoid relying on debt for unexpected expenses. Building an emergency fund is a critical component of a sound financial plan. This fund acts as a safety net, providing a cushion for unforeseen circumstances like job loss, medical emergencies, or car repairs.

- Set a savings goal:Determine a realistic amount you can save each month, even if it’s a small amount. Consistency is key. Consider automating your savings by setting up regular transfers from your checking account to your savings account.

- Track your spending:Monitor your spending habits to identify areas where you can cut back. Use budgeting apps, spreadsheets, or a simple notebook to track your income and expenses.

- Prioritize needs over wants:Differentiate between essential needs and non-essential wants. Focus on meeting your basic needs first before indulging in discretionary spending.

- Look for ways to save:Explore opportunities to reduce your expenses. This could include negotiating lower bills, taking advantage of discounts, or finding cheaper alternatives for goods and services.

Responsible Credit Card Usage

Credit cards can be a valuable tool for building credit, but they can also lead to debt accumulation if not used responsibly. Responsible credit card usage involves understanding your credit limit, making timely payments, and avoiding excessive spending.

- Pay your balance in full each month:Avoid carrying a balance on your credit card as much as possible. This prevents interest charges from accruing and helps you manage your debt effectively.

- Keep your credit utilization low:Aim to keep your credit utilization ratio (the amount of credit you use compared to your available credit) below 30%. A lower ratio generally indicates better creditworthiness.

- Avoid cash advances:Cash advances often come with high interest rates and fees. Use your credit card for purchases and avoid using it as a source of cash.

- Shop around for the best rates:Compare credit card offers from different institutions to find the lowest interest rates and fees.

Seeking Professional Help

Sometimes, managing debt on your own can feel overwhelming. If you’re struggling to make progress or feel like you’re losing control, seeking professional help can provide valuable guidance and support.

Types of Professional Help

There are two main types of professionals who can assist you with debt management: credit counseling agencies and financial advisors.

- Credit Counseling Agencies:These non-profit organizations offer free or low-cost services to help individuals manage their debt. They can provide personalized advice, develop a debt management plan, and negotiate with creditors on your behalf. Some agencies may offer debt consolidation programs, where you combine multiple debts into a single loan with a lower interest rate.

- Financial Advisors:These professionals can provide comprehensive financial planning services, including debt management strategies. They can help you create a budget, identify areas where you can cut expenses, and develop a plan to pay down your debt. While financial advisors may charge fees for their services, they can offer valuable insights and personalized guidance based on your unique financial situation.

Benefits of Seeking Professional Help

- Objectivity:Professionals can provide an unbiased perspective on your financial situation, helping you make informed decisions without emotional biases.

- Negotiation Expertise:Credit counselors and financial advisors have experience negotiating with creditors and may be able to secure more favorable terms than you could on your own.

- Accountability:Having a professional involved can provide accountability and motivation to stick to your debt management plan.

- Stress Reduction:Dealing with debt can be stressful. Professionals can offer support and guidance, reducing your anxiety and helping you regain control of your finances.

Signs You Need Professional Help

- You’re constantly struggling to make minimum payments:If you’re struggling to keep up with your minimum payments, it’s a sign that your debt is becoming unmanageable.

- You’re using credit cards to pay for essential expenses:Using credit cards to cover basic needs like groceries or rent is a clear indication that you’re in over your head.

- You’re feeling overwhelmed and stressed about your finances:Debt can significantly impact your mental and emotional well-being. If you’re constantly worried about your finances, it’s time to seek help.

- You’ve tried to manage your debt on your own without success:If you’ve been trying to manage your debt independently but haven’t seen significant progress, professional assistance may be necessary.

Wrap-Up

By understanding your debt, creating a plan, and building responsible financial habits, you can take control of your financial future. Remember, managing debt is an ongoing process that requires discipline and commitment. Don’t hesitate to seek professional help when needed, as a financial advisor can provide valuable guidance and support.

Top FAQs

What is the best way to pay off debt quickly?

The most effective approach depends on your individual circumstances. The debt snowball method focuses on paying off smaller debts first to gain momentum, while the debt avalanche method prioritizes debts with the highest interest rates.

Can I get my debt forgiven?

Debt forgiveness is possible in certain situations, such as through bankruptcy or government programs. However, it’s crucial to explore all options carefully and understand the potential consequences.

What if I can’t afford my minimum payments?

If you’re struggling to make minimum payments, contact your creditors immediately. They may be willing to work with you on a payment plan or offer temporary hardship assistance.