Difference Between Financial Intelligence and Financial Literacy: A Detailed Analysis

Difference between financial intelligence and financial literacy sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with casual formal language style and brimming with originality from the outset.

Financial intelligence and financial literacy are two crucial concepts that often get intertwined in discussions about personal finance. Understanding the distinctions between these terms is essential for anyone looking to navigate the complexities of managing finances effectively. In this detailed analysis, we delve into the nuances of financial intelligence and financial literacy, shedding light on their unique characteristics and importance in financial decision-making.

Understanding Financial Intelligence vs. Financial Literacy

Financial intelligence and financial literacy are two crucial concepts in managing one’s finances effectively. While they are related, they have distinct differences that are important to understand.

Financial intelligence refers to the ability to analyze financial situations, make informed decisions, and understand complex financial concepts. It involves critical thinking, problem-solving skills, and the ability to adapt to changing financial circumstances. In essence, financial intelligence is about understanding the bigger picture of how money works and how to leverage financial opportunities.

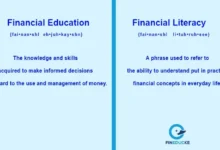

On the other hand, financial literacy is the knowledge and understanding of basic financial concepts such as budgeting, saving, investing, and managing debt. It focuses on the practical skills needed to navigate everyday financial decisions and tasks. Financial literacy is about having a foundational understanding of personal finance principles to make sound financial choices.

Key Differences

- Financial intelligence involves deeper analysis and critical thinking, while financial literacy focuses on basic financial knowledge and skills.

- Financial intelligence is about understanding complex financial concepts and strategies, while financial literacy deals with practical money management skills.

- Financial intelligence helps in long-term financial planning and wealth building, whereas financial literacy aids in day-to-day financial decision-making.

Examples

- Financial intelligence may involve analyzing market trends, evaluating investment opportunities, and creating a comprehensive financial plan for retirement.

- Financial literacy, on the other hand, includes creating a budget, understanding interest rates, and knowing how to use credit cards responsibly.

Importance of Financial Intelligence and Financial Literacy

Financial intelligence and financial literacy are both crucial aspects of managing personal finances effectively. While financial literacy provides individuals with the basic knowledge and understanding of financial concepts, financial intelligence goes a step further by enabling individuals to apply that knowledge in making informed and strategic financial decisions.

Financial intelligence is essential for making informed financial decisions because it involves the ability to analyze and interpret financial information effectively. By understanding complex financial concepts and being able to assess the potential risks and rewards of different financial decisions, individuals can make sound choices that align with their long-term financial goals. This can lead to better investment decisions, effective budgeting, and overall financial stability.

On the other hand, financial literacy plays a key role in helping individuals manage their finances effectively on a day-to-day basis. It equips individuals with the knowledge and skills needed to create budgets, manage debt, save for the future, and navigate the financial landscape with confidence. Without a basic level of financial literacy, individuals may struggle to make sound financial decisions and may be more vulnerable to financial pitfalls such as debt, overspending, or inadequate savings.

In real-life scenarios, financial intelligence can be seen in action when individuals are able to analyze investment opportunities, assess the risks involved, and make strategic decisions that lead to financial growth. For example, a financially intelligent individual may successfully diversify their investment portfolio to minimize risk and maximize returns.

On the other hand, financial literacy is evident when individuals are able to create and stick to a budget, manage their expenses effectively, and make informed decisions about borrowing and saving. For instance, a financially literate individual may be able to prioritize their financial goals, such as saving for retirement or a major purchase, and take the necessary steps to achieve them.

Overall, both financial intelligence and financial literacy are essential components of financial success, with each playing a unique role in helping individuals navigate the complexities of personal finance and achieve their long-term financial goals.

Development of Financial Intelligence and Financial Literacy

Financial intelligence and financial literacy can be developed and improved over time through various strategies and methods. By continuously enhancing these skills, individuals can make better financial decisions and secure their financial future.

Strategies to Enhance Financial Intelligence

- Read books and articles on financial management and investment to gain knowledge about different financial concepts and strategies.

- Attend seminars, workshops, or online courses to learn from experts in the field and stay updated on the latest trends in finance.

- Practice analyzing financial statements and understanding key financial ratios to improve your ability to assess the financial health of companies.

- Engage in discussions with financial advisors or mentors to gain insights and perspectives on complex financial matters.

Methods to Improve Financial Literacy

- Create a budget and track your expenses to develop a better understanding of your financial habits and identify areas for improvement.

- Learn about different types of investments, such as stocks, bonds, and mutual funds, to diversify your portfolio and maximize returns.

- Understand the basics of taxes, insurance, and retirement planning to make informed decisions that align with your long-term financial goals.

- Utilize financial management tools and apps to monitor your financial progress and make adjustments as needed.

Tips for Continuous Development of Financial Intelligence and Literacy

- Set specific financial goals and regularly review your progress to stay motivated and focused on improving your financial knowledge.

- Seek feedback from professionals or experts in the financial industry to gain valuable insights and advice on how to enhance your financial skills.

- Network with like-minded individuals who are also interested in improving their financial intelligence and literacy to exchange ideas and experiences.

- Stay curious and open-minded about learning new financial concepts and strategies to adapt to changing economic conditions and market trends.

Application of Financial Intelligence and Financial Literacy

Financial intelligence and financial literacy play crucial roles in making informed financial decisions and managing personal finances effectively. Let’s delve into how these concepts can be applied in practical scenarios to achieve financial goals.

Financial Intelligence in Investment Decisions

Financial intelligence involves analyzing and interpreting financial information to make informed decisions. When it comes to investment decisions, individuals with high financial intelligence can:

- Evaluate investment opportunities by conducting thorough research on market trends, company performance, and potential risks.

- Analyze financial statements and ratios to assess the profitability and stability of investments.

- Diversify their investment portfolio to minimize risks and maximize returns.

- Utilize strategies like dollar-cost averaging and asset allocation to optimize investment outcomes.

- Adjust investment decisions based on changing market conditions and economic factors.

Financial Literacy in Budgeting and Saving

Financial literacy is essential for effective budgeting and saving practices. Individuals with strong financial literacy can:

- Create a realistic budget by tracking income, expenses, and identifying areas for saving.

- Understand the importance of emergency funds and long-term savings goals for financial stability.

- Utilize tools like spreadsheets or budgeting apps to monitor spending habits and identify opportunities for cost-cutting.

- Implement strategies like automatic transfers to savings accounts and setting financial goals to enhance saving habits.

- Evaluate different savings options like high-yield savings accounts or investment vehicles to grow wealth over time.

Collaboration of Financial Intelligence and Financial Literacy

Both financial intelligence and financial literacy complement each other to achieve overall financial well-being. By combining these concepts, individuals can:

- Make well-informed investment decisions based on a deep understanding of financial markets and personal financial goals.

- Implement effective budgeting and saving strategies to ensure financial stability and achieve long-term objectives.

- Adapt to changing economic conditions and market trends by leveraging financial intelligence to make informed adjustments to investment and saving plans.

- Work towards building wealth and financial security by applying both financial intelligence and financial literacy in a coherent and strategic manner.

Final Thoughts

In conclusion, the difference between financial intelligence and financial literacy is not just a matter of semantics but a fundamental aspect of financial education. By grasping the intricacies of both concepts and actively working towards enhancing both aspects, individuals can empower themselves to make sound financial decisions and secure their financial future.